Impact of COVID-19 on Business Valuations – The New Normal

Impact of Covid-19 on Business Valuations

The Covid-19 pandemic that resulted in the forced closure of many businesses throughout the United States beginning in mid-March has created many challenges for appraisers engaged to value businesses for SBA 7a business acquisition loans. In conjunction with President Trump’s 15 Days to Slow the Spread initiative on March 16, 2020, recommendations from the White House Coronavirus Task Force and CDC guidelines, many state governors declared states of emergency and issued shelter in place/stay at home/home or work/safer at home orders. Most non-essential businesses were forced to close while other businesses such as restaurants were required to alter operations significantly. Large portions of the United States’ economy shut down or reduced operations as a result of the governors’ orders. This situation lasted throughout the month of April and into mid-May when some governors began to ease restrictions and begin the process of reopening their economies.

At the outset of the pandemic and state closures, it was unclear how long the pandemic would last, how long and how many states would be under shelter in place or similar lockdown orders, and how the economy would be impacted. At the outset, it was widely anticipated that the pandemic would last many weeks and possibly many months. Most experts agreed that the economy would be negatively impacted in the short-term and that there would be significant long-term economic consequences. Many businesses faced extended periods of closure or limited operations. Even businesses not forced to close or limit operations to help slow the spread experienced reduced activity due to lower demand for goods and services from consumers staying at home and other businesses closed or partially closed. Nearly all businesses, both essential and non-essential, were concerned about how they would be impacted by the pandemic. Business uncertainty was high. In short, everyone was expecting a downturn in economic and business activity due to the pandemic. The questions to which no one had answers were: How long will the closures last? When will we get back to normal?

As of the writing of this article in early June, most states have started to reopen or at least ease restrictions, though many still have certain restrictions on businesses and operations despite plans for the gradual reopening of their economies in phases. However, some of the same questions facing business owners at the outset remain today, even as restrictions are easing and the economy is reopening. Businesses still don’t know how long the pandemic will last and how it will impact their revenue generating ability and operations over the next year. The timing of a return to full operations as opposed to limited operations remains up-in-the-air. With the possibility of a resurgence of the virus in the third or fourth quarter or even into 2021, will businesses be forced to close again if some states impose shelter in place/lockdowns or closures again? Out of precaution, will businesses be forced to adjust operations until a vaccine is developed? Will we get back to normal or will we adjust and adapt to a new normal?

Appraisers tasked with valuing businesses using a valuation date during the closure period face similar questions and uncertainty. The answer to many of the aforementioned questions were not known or knowable to the appraiser as of the valuation date. For example, an appraiser valuing a restaurant operating at limited capacity as of April 1, 2020 has absolutely no way of knowing how long the shelter in place or lockdowns will last, when the economy will reopen, exactly how these factors will impact the company’s financial performance, how long the company’s financial performance will be negatively impacted, and what long-term changes to operations, if any, may result from the pandemic. As of April 1, 2020, people are scared about the pandemic and how it will affect the United States, the economy, and businesses. No one has any clarity regarding the future, and no one can divine how the pandemic and its impact on business will play out. In reality, we know very little about the virus and how it will impact businesses and the economy in the long-term during the extended period of state closures/shelter in place/lockdowns. As of April 1, 2020, we know there is considerable uncertainty, but we don’t know the extent to which the economy and businesses will be impacted. We know that many non-essential businesses forced to close will be negatively impacted financially. We know that some essential businesses will also be negatively impacted as a result. However, we know that some essential businesses will likely benefit from the closures and the pandemic. We can only hypothesize the answer to many of these questions and uncertainties.

For lenders attempting to close SBA 7a loans over the last couple months, the outlook has been equally uncertain. Opportunities for closing deals was limited during state shelter in place orders/lockdowns and remain limited today. Even now with many states having reopened, there is considerable uncertainty regarding the sales of businesses and the ability to finance those transactions due to the pandemic’s impact. Lenders and businesses are questioning how business values have been and will be impacted by the pandemic. They also want to know how appraisers will address this in valuations. These concerns are shared by many in the appraisal community, but there is no clear consensus regarding how to address the pandemic from a technical perspective in the appraisal assignment. This discussion offers our thoughts on this matter.

We believe that the Covid-19 pandemic is a ‘Black Swan’ event. Investopedia explains a black swan event as follows:

A black swan is an unpredictable event that is beyond what is normally expected of a situation and has potentially severe consequences. Black swan events are characterized by their extreme rarity, their severe impact, and the widespread insistence they were obvious in hindsight

- A black swan is an extremely rare event with severe consequences. It cannot be predicted beforehand, though many claim it should be predictable after the fact.

- Black swan events can cause catastrophic damage to an economy, and because they cannot be predicted, can only be prepared for by building robust systems.

- Reliance on standard forecasting tools can both fail to predict and potentially increase vulnerability to black swans by propagating risk and offering false security.

The Covid-19 pandemic has created considerable uncertainty regarding the short-term outlook for the economy and business activity and the recovery period for the broader economy. No one can project or predict the magnitude of the short-term economic consequences resulting from the pandemic. However, we believe that the long-term prospects for the United States’ economy remain favorable after the Covid-19 pandemic ends, and we’re starting to see an uptick in economic activity now that many states are easing restrictions and lifting shelter in place/lockdown orders. From a long-term perspective, this black swan event is likely to have a transitory impact on the economy and business values. Ultimately, we believe this is a blip on the radar of the long-term economy. The pandemic will end at some point. People will go back to work and get on with their lives. Businesses will resume operations. The economy will get back to normal.

It is still too early to tell if there will be any lasting changes in terms of prolonged social distancing, wearing masks in public, etc. It is inconceivable to us that businesses will be forced to operate at significantly reduced capacities in perpetuity. Restaurants aren’t going to permanently close their dining rooms and do just take out. Likewise, they aren’t going to permanently operate at 25% capacity. Retailers are not going to be permanently forced to limit the number of shoppers in their store at one time. Entertainment venues, casinos, and theme parks are not going to perpetually operate at 20-30% capacity. Football and baseball games are not going to be played in empty stadiums for the rest of our lives. The temporary adjustments made during the pandemic to stop the spread of Covid-19 are not going to remain in perpetuity. We will eventually return to normal, not some altered reality where we live the rest of our lives always six feet apart from others, always wearing masks and always separated from others by plexiglass.

What does all of this mean from a valuation perspective? Challenging times for sure! At the heart of the valuation of a business lie two fundamental concepts…cash flow and risk. Capitalizing net cash flow by a risk adjusted rate of return (reflecting risk factors) is one of the most common methods of valuing a business for lending purposes. This is known as the capitalization of earnings method and is usually applied to businesses that exhibit stable financial performance and cash flow. Generally, an examination of historic performance or a weighted average of historic performance of the business is used to develop an estimate of expected/normalized cash flow in perpetuity. The proxy of normalized, on-going cash flow is then capitalized by the risk adjusted rate of return, usually derived from the weighted average cost of capital (WACC) less the long-term sustainable growth rate.

The cost of equity component of the weighted average cost of capital is usually developed using a build-up method which adds various risk premia over the risk-free rate. The risk premium represents the incremental rate of return demanded by an investor to compensate for the investment opportunity’s risk over and beyond the risk-free rate and that of comparable investments. The cost of equity can be developed by adding the following factors to the risk-free rate of return (usually derived from the 20 year yield on US Treasury bonds): the equity risk premium, the small company size premium, the industry risk premium and the company specific risk premium.

Investing in a small business is inherently risky. Each small business has different risk characteristics. Investors or buyers of these businesses are compensated for this risk via a higher rate of return in the form of the company specific risk premium. This is a subjective risk premium based on the appraiser’s judgment, assessment of risk factors and analysis of total risk and return. Factors that an appraiser may consider in developing the company specific risk premium include: the business’s financial situation, the long-term outlook and stability of the industry, the depth of the company’s management and the importance of key personnel, competition and competitive factors, the historical trend in the company’s earnings/margins/financial structure, the company’s location/geographic region, product/service diversification, customer concentration, and financial risk.

Why is this all important to this discussion? Conceptually, appraisers can account for the pandemic’s impact on the value of a business in two ways: 1) consideration of the impact on the company’s cash flow, or 2) an adjustment to the risk profile via the company specific risk premium. To illustrate the possibilities and how this may impact a valuation, we will provide three examples using the same company. This represents an actual valuation that was performed prior to the Covid-19 pandemic. We then update the analysis using two scenarios: the value developed once the pandemic was known using an increased company specific risk premium to account for the business closure and the value developed using assumptions regarding reduced cash flow from the business closure and the company specific risk premium.

Please note that this is a simplistic example used to illustrate the possible ways an appraiser can address the pandemic’s impact on the value of a business for valuation dates prior to and during the pandemic and shutdowns. Ultimately, an appraiser must use reasoned and informed judgement considering the case-specific facts and circumstances surrounding the business in developing an opinion of value . This is not a recommendation to use any particular approach or method for a specific assignment. This is simply an illustration of how various scenarios may or may not impact the value of a business and offers appraisers potential adjustments to consider in these challenging valuation times.

The simplistic example that follows is centered around both non-essential and essential businesses that were negatively impacted by the state shelter in place/lockdowns such as hair salons, restaurants, daycare, retailers, dry cleaners, liquor stores, and the many other businesses forced to close, reduce operations, or cut activity due to decreases in demand for their goods or services . To be sure, there are essential businesses that have benefited from the closures and that continue to benefit from the pandemic. Companies that produce or sell goods for healthcare workers, sanitizing products, grocers, pizza delivery restaurants, etc. have seen increased activity in many cases. The risk factors, outlook and sustainable cash flow would be different for essential businesses and those that benefited from the closures compared to the risk factors of businesses closed or operating at reduced capacities.

Scenario #1: Pre-Covid-19 Pandemic

The calculation of the company’s weighted average adjusted free cash flow is presented below. This scenario pre-dates the Covid-19 pandemic; no consideration has been given to the effects of the pandemic on the business as the partial period for 2020 represents the time period prior to the pandemic affecting business in the United States. State shelter in place/lockdowns/closures didn’t start until mid-March. The shelter in place/lockdowns/closures weren’t known or knowable as of the end of February.

The following table calculates the capitalization rate for the Company. The company specific risk premium of 10% represents the assumptions made based on information known and facts and circumstances that existed prior to the Covid-19 pandemic.

The following table illustrates the calculation of the enterprise fair market value using the capitalization of earnings method in the pre-Covid 19 environment.

Scenario #2: Risk Premium Adjustment to Account for Covid-19 Pandemic Effects

For illustration purposes in this scenario, we will assume the valuation date is April 1, 2020. At that time, there was considerable uncertainty regarding the duration of the shutdowns and the impact on the economy and the company. In the absence of a crystal ball, it would have been impossible to predict the actual impact on the business’s cash flow. The scenario assumes that the Company’s historic performance before the Covid-19 pandemic is representative of the Company’s normalized performance and that the effects of the pandemic are transitory. The risk is being accounted for by increasing the company specific risk premium.

The following table calculates the capitalization rate. In this scenario we have adjusted the company specific risk premium to 20% to account for the uncertainty of the company’s financial performance created by the Covid-19 pandemic. In addition to the many factors already considered in assessing the company specific risk premium, the appraiser may consider additional factors resulting from the Covid-19 pandemic that may contribute to an incremental increase in the company specific risk premiums. These additional risk considerations may include capacity constraints, lack of demand, consumer habits/changes to habits, potential regulatory changes (good or bad), supply chain issues, cost increases due to precautionary measures, additional staffing requirements, incremental financial risk stemming from weak cash flow, etc.

Some businesses, such as restaurants, bars or theaters, may be more impacted by this analysis than others, such as liquor stores or manufacturers. Some businesses may not be impacted at all or only marginally impacted such as convenience stores, professional service firms, etc. The analysis will be case specific based on the circumstances surrounding the business being valued. There is no blanket incremental increase in the risk premium. Many of the factors to be considered cannot be quantified and remain at the judgment/discretion of the appraiser using reasoned and informed judgment.

As a result of the increased company specific risk premium, the weighted average cost of capital increased to 11.7% as compared to the pre-pandemic weighted average cost of capital of 10.4%.

The calculation of the enterprise fair market value is illustrated in the table below. Due to the Covid-19 pandemic, this also assumes that the liquidity (marketability) of the business being valued has decreased thus requiring a higher marketability discount. (This is a separate topic for another discussion.)

Scenario #3: Cash Flow Adjustment to Account for Covid-19 Pandemic Effects

Using the discounted cash flow method, the appraiser must determine the company’s net free cash flow base as of the date of valuation, April 1, 2020 for purposes of this discussion. This scenario assumes that the company will realize no cash flow in the twelve months following the valuation date due to closures/limited operations/reduced financial performance due to economic weakness created by the Covid-19 pandemic. Following this, the company will return to a normalized level of financial performance based on the historic financials.

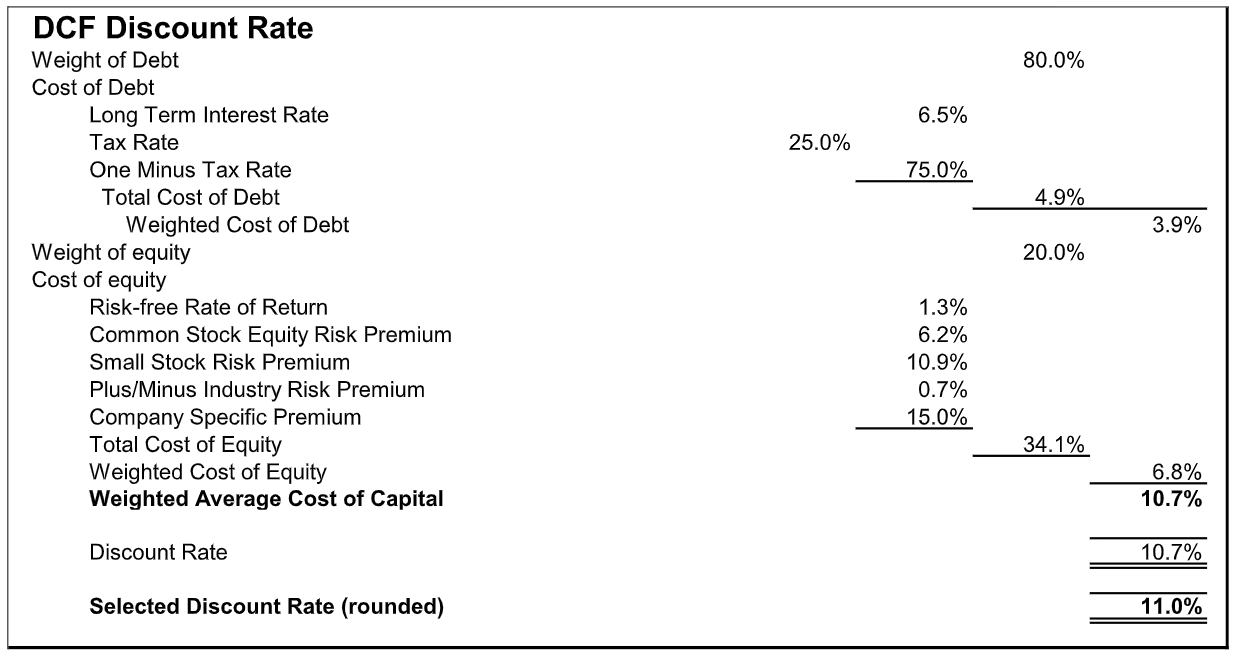

The following table calculates the weighted average cost of capital, which will be used as the discount rate. The company specific risk premium is higher than the pre-pandemic environment but lower than the previous scenario which adjusted only the company specific risk premium. As a result, the weighted average cost of capital is estimated at 11%; this is higher than the pre-pandemic weighted average cost of captial but lower than under the scenario where the risk was accounted for only by increasing the company specific risk premium.

The following exhibit shows the estimated projected earnings for the forecast period after the date of valuation discounted to their present values. In addition, the last year’s projected earnings were capitalized into a residual value and discounted to its present value.

Conclusions

The following table illustrates the value indications produced by each of the previous scenarios. As can be seen in the table, the value conclusions are relatively similar when adjusting only the company specific risk premium to account for increased risk stemming from the pandemic and when attempting to project financial performance in the short-term using the discounted cash flow method. In this simplistic example, these two scenarios produce similar results. Different assumptions regarding future cash flow and the time of future cash flow would increase the differential between the methods. What is clear is that both these methods produce values that reflect a roughly 25% reduction in value from pre-Covid values. Again, differing assumptions would yield different values.

It is important to note that this decline in value is a function of the here and now. Should the company in the example return to normal operations quickly and should the US economy experience a ‘V’ shaped recovery, the fair market value in the future would likely rise towards the normal pre-Covid value estimate. The gap between the post Covid-19 values and the pre-Covid value will likely close if the business is able to return to financial performance similar to historic norms. If the recovery is ‘U’ shaped, the timing of the convergence of values towards the pre-Covid levels may be extended. If the virus has a resurgence in the second half of 2020 or in 2021 and there are future closures, the values may remain depressed for an extended period.

There is no single “right way” for an appraiser to account for the impact of the Covid-19 pandemic in a business valuation with a valuation date after the pandemic began. Our scenarios above are offered for consideration and comparison. They represent simplistic examples. Appraisers ultimately bear the responsibility of preparing an analysis and reaching an opinion of value that is based on facts and circumstances known or knowable at the valuation date and reasonable, informed judgment. There will be disagreements over how to address the impact of the Covid-19 pandemic in business valuations. However, we believe this is largely a short-term challenge. Life and business will eventually return to normal, though there may be some short-term changes to lifestyles, habits, and behaviors. Months from now, we may very well look back on this and say the shutdowns had less long-term economic and valuation consequences than initially anticipated. Time will tell if there are any lasting changes to our daily lives, work, habits, business, the economy, and valuations. For now, appraisers must address these challenges in the most feasible and reasonable ways possible.